Is a Bond Allocation Really an Adequate Diversifier?

September 2022

ShareURL Copied!

Key Takeaways

The historically low correlation between stocks and bonds may provide ballast for a portfolio when equity markets decline. But the inverse relationship between stocks and bonds may be more tenuous than many realize.

With both asset classes having benefitted from the low interest rate environment, there is increased risk they could suffer in tandem as the

Federal Reserve raises rates.

By including solutions that are designed to be uncorrelated to both equity and fixed income, investors may be better equipped to navigate a market environment in which the performance of their entire stock and bond portfolio is correlated to interest rate risk.

In traditional portfolio models, fixed income commands a sizable allocation for one reason: diversification. The historically low correlation between stocks and bonds may provide ballast for a portfolio and reduce drawdowns when equity markets decline.

But the inverse relationship between stocks and bonds may be more tenuous than many investors realize and may potentially be on particularly shaky ground today. That doesn’t bode well from a diversification standpoint and underscores the need for investors to consider adding other asset classes and strategies that have been uncorrelated to both stocks and bonds, to their portfolio.

This article addresses the reasons why fixed income may not be providing the diversification investors expect, and what investors can do to improve portfolio outcomes.

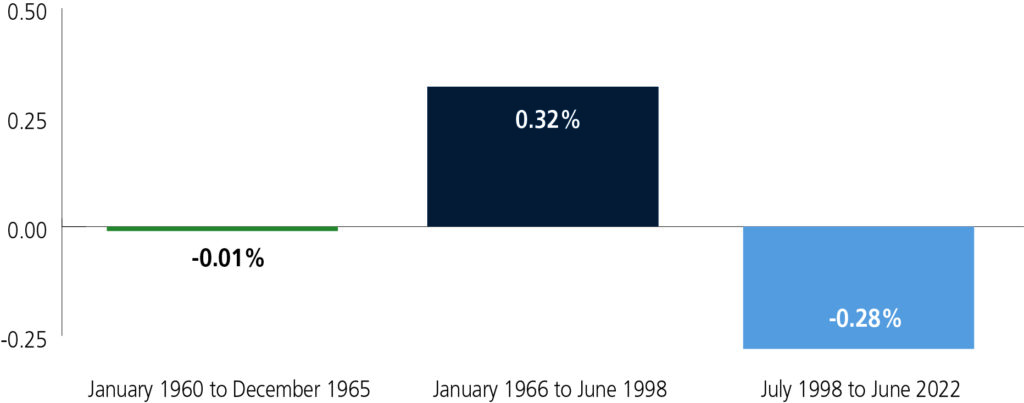

A Look Back: Stocks and Bonds Are Not Always Uncorrelated

For the past 20 years, stock and bond performance has been negatively correlated, but that has not been the case in every market cycle. During the previous 30 years, stocks and bonds were positively correlated.

Stock and Bond Correlation: Negative and Positive Regimes

Source: LoCorr Fund Management. Data as of June 30, 2022. Correlation: S&P 500 Index with 10-Year US Treasury Index.

The fact that different correlation environments exist suggests that fixed income shouldn’t be counted on as the only long-term solution for hedging equity market risk. Can bonds still bring the diversification to a portfolio that they have provided in the past?

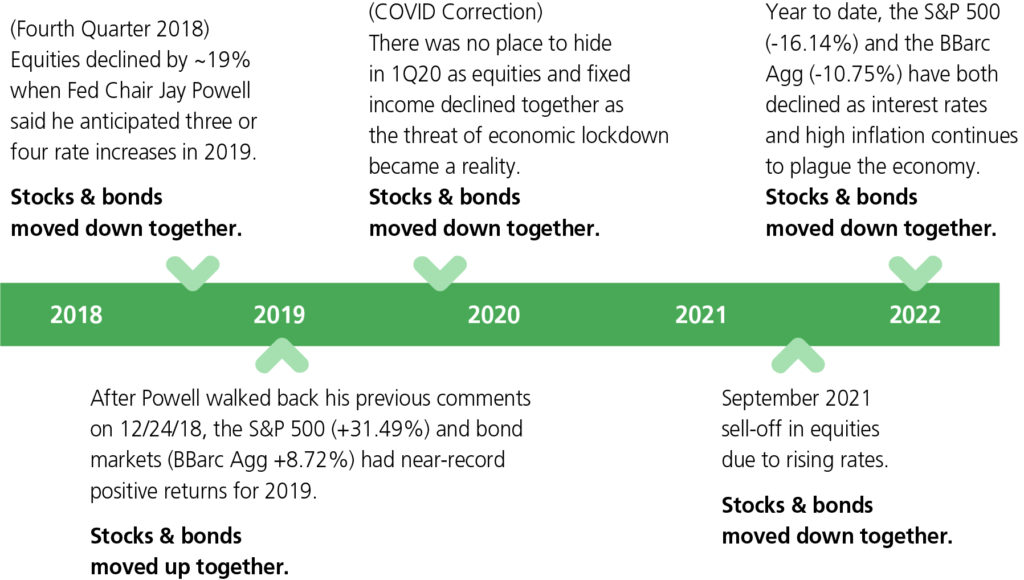

Recent Periods – Bonds Failed to Provide the Diversification Investors Expect

The Interest Rate Outlook Guides Everything

It is impossible to assign stock market movement to a single factor, but many attribute the stock market’s recent bull run to low interest rates, and it’s even more recent decline to higher interest rates. Surging inflation has contributed to the Federal Reserve’s aggressive stance on raising rates to combat inflation. Recent comments by members of the Federal Reserve have indicated that interest rates should continue to rise and will need to remain elevated in order to bring inflation back down.

The changing composition of standard indices such as the S&P 500 makes stocks even more sensitive to interest rates. In recent years, growth stocks have become a larger segment within the index. Many of these stocks disproportionately benefit from a low interest rate regime because it allows their future earnings to be discounted at lower rates which leads to higher valuations. These high valuations may be particularly vulnerable as investors begin discounting higher interest rates, the cost of borrowing increases, etc.

Equity markets’ sensitivity to interest rates is problematic for portfolio diversification because rates are already one of the biggest risk factors for fixed income. With both asset classes having benefitted from the low interest rate environment, there is increased risk they could suffer in tandem as the Federal Reserve raises rates.

Greater Diversification Is Needed

In response, investors must consider new strategies and asset classes that are uncorrelated to both equity and fixed income. In the past 10 to 15 years, an increasing number of low-correlating strategies and asset categories have opened to individual investors. This provides an opportunity to assemble a dedicated sleeve of non-traditional investments, that are uncorrelated to stocks and bonds, and also uncorrelated to each other.

Importantly, many of these strategies are ‘directionally agnostic,’ meaning they can generate positive returns (or losses) in both falling and rising markets. This means the strategies offer the potential to provide positive performance in times when stocks and bonds lag, but also when they perform well.

By blending these strategies with a traditional equity and fixed income allocation, advisors and their clients may be better equipped to navigate a market environment in which the performance of their entire stock and bond portfolio is correlated to interest rate risk.

S&P 500 Index is a capitalization weighted unmanaged benchmark index that includes the stocks of 500 large capitalization companies in major industries. This total return index includes net dividends and is calculated by adding an indexed dividend return to the index price change for a given period. SBBI U.S. Long Government Bond Index measures the performance of a single issue of outstanding US Treasury bond with a maturity term of around 21.5 years. It is calculated by Morningstar and the raw data is from Wall Street Journal.

Past Performance does not guarantee future results. Index performance is not indicative of fund performance. For current standardized fund performance, please call 1.855.LCFunds or visit www.LoCorrFunds.com. The performance of various indices is shown for comparison purposes only. The performance of those indices was obtained from published sources believed to be reliable, but which are not warranted as to accuracy or completeness. Unless noted otherwise, index returns do not reflect fees or transaction costs and reflect reinvestment of net dividends. One cannot invest directly in an index.

The Fund’s investment objectives, risks, charges, and expenses must be considered carefully before investing. The prospectus contains this and other important information about the investment company, and it may be obtained by calling 1.855.LCFUNDS, or visiting www.LoCorrFunds.com. Read it carefully before investing.

Mutual fund investing involves risk. Principal loss is possible. The Funds are non-diversified, meaning it may concentrate its assets in fewer individual holdings than a diversified fund. Therefore, the Funds are more exposed to individual stock volatility than a diversified fund. The Funds invest in foreign investments and foreign currencies which involve greater volatility and political, economic and currency risks and differences in accounting methods. These risks are greater for emerging markets. The Funds may make short sales of securities, which involves the risk that losses may exceed the original amount invested. Investing in commodities may subject the Funds to greater risks and volatility as commodity prices may be influenced by a variety of factors including unfavorable weather, environmental factors, and changes in government regulations. Investing in derivative securities derive their performance from the performance of an underlying asset, index, interest rate or currency exchange rate. Derivatives can be volatile and involve various types and degrees of risks, and, depending upon the characteristics of a particular derivative, suddenly can become illiquid. Derivative contracts ordinarily have leverage inherent in their terms which can magnify the Fund’s potential for gains or losses through increased long and short position exposure. The Fund may access derivatives via a swap agreement. A risk of a swap agreement is the risk that the counterparty to the agreement will default on its obligation to pay the Fund. Investments in debt securities typically decrease in value when interest rates rise. This risk is usually greater for longer-term debt securities. Investments in Asset Backed, Mortgage Backed, and Collateralized Mortgage-Backed Securities include additional risks that investors should be aware of such as credit risk, prepayment risk, possible illiquidity and default, as well as increased susceptibility to adverse economic developments. The LoCorr Long/Short Equity Fund may invest in small- and medium-capitalization companies which involve additional risks such as limited liquidity and greater volatility. The Fund may also invest in lower-rated and non-rated securities which present a greater risk of loss to principal and interest than higher-rated securities. ETF investments are subject to investment advisory and other expenses, which will be indirectly paid by the Fund. As a result, the cost of investing in the Fund will be higher than the cost of investing directly in ETFs and may be higher than other mutual funds that invest directly in stocks and bonds. ETFs are subject to specific risks, depending on the nature of the ETF. The Spectrum Income Fund’s portfolio will be significantly impacted by the performance of the real estate market generally, and the Fund may be exposed to greater risk and experience higher volatility than would a more economically diversified portfolio. Property values may fall due to increasing vacancies or declining rents resulting from economic, legal, cultural, or technological developments. Investments in Limited Partnerships (including master limited partnerships) involve risks different from those of investing in common stock including risks related to limited control and limited rights to vote on matters affecting the Limited Partnership, risks related to potential conflicts of interest between the Limited Partnership and the Limited Partnership’s general partner, cash flow risks, dilution risks and risks related to the general partner’s limited call right. Underlying Funds are subject to management and other expenses, which will be indirectly paid by the Fund.

Click here for important disclosure and definition information.

Mutual fund investing involves risk. Principal loss is possible.

The Fund’s investment objectives, risks, charges and expenses must be considered carefully before investing. The prospectus contains this and other important information about the investment company, and it may be obtained by clicking here or a free-hard copy is available by calling 1.855.LCFUNDS. Read it carefully before investing.

The Funds are offered only to United States residents, and information on this site is intended only for such persons. Nothing on this website should be considered a solicitation to buy or an offer to sell shares of the Funds in any jurisdiction where the offer or solicitation would be unlawful under the securities laws of such jurisdiction.

The LoCorr Funds are distributed by Quasar Distributors, LLC.

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful.

Strictly Necessary Cookies

Strictly Necessary Cookie should be enabled at all times so that we can save your preferences for cookie settings.

If you disable this cookie, we will not be able to save your preferences. This means that every time you visit this website you will need to enable or disable cookies again.