Inflation Risk: Persistent or Transitory is the Wrong Question

May 2022

ShareURL Copied!

Key Takeaways

Instead of wondering whether inflation is a persistent or transitory threat, a better question is whether your client’s portfolio is prepared for it.

Advisors can modernize portfolios by including asset classes and strategies that are uncorrelated to stocks and bonds, and are resilient to different market conditions and risks.

Proper diversification is a constant mindset, not a reaction. By including a blend of low-correlating strategies, advisors may create a client experience with better outcomes and is easier to manage.

Persistent … or transitory? It’s the inflation question that has been weighing on the markets over the last year. As each economic data point trickles out, it is analyzed and re-analyzed, with that focus in mind. But it may be the wrong question to ask.

Instead of pondering whether inflation is a real threat, a more pertinent question is whether your clients’ portfolios are prepared for it. Too often, the answer is no. This is because the average portfolio is not well suited for handling a variety of adverse market conditions. And over the last decade plus, they haven’t needed to be.

Most advisors and allocators continue to build 60/40 or 70/30 stock and bond portfolios. These standard allocation models have worked well since the 2008 financial crisis when the most important investment decision was simply to stay off the sidelines, maintain an allocation to stocks and bonds, and let a market rebound and falling interest rates take care of the rest.

But the threat of inflation, and rising interest rates that would eventually follow, serve as a cautionary reminder that market conditions change and old threats often re-emerge.

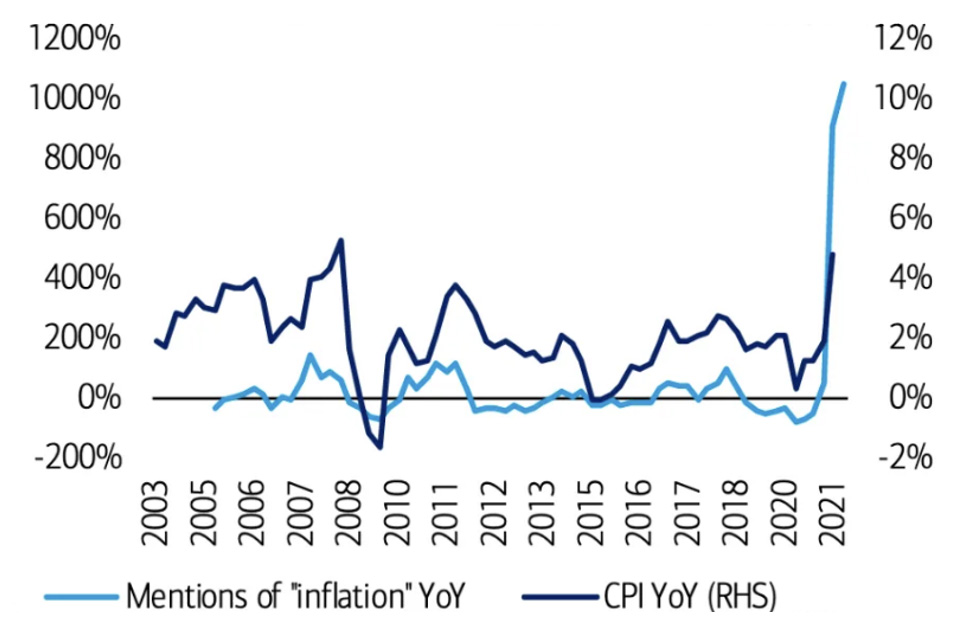

Inflation Concerns Mount

Mentions of inflation during S&P companies’ earnings calls have risen over 1000% year over year.

Source: BofA Global Research, Bloomberg, 2003-6/30/21. Consumer Price Index year over year is represented on the right hand side of the graph.

As the chart shows, inflation is a growing concern. Instead of gauging whether the threat is real, investors may benefit from proactively building a portfolio that can better withstand it.

Advisors can prepare portfolios by including asset classes and strategies that are uncorrelated to stocks and bonds, and are resilient to different market conditions and risks.

For example, in an inflationary environment, commodities or real estate can help buffer against – and even benefit from – inflation. To protect against rising rates, advisors and their clients could seek out alternative income strategies that are uncorrelated to bonds yet still offer the potential to deliver high income. Better yet, combining several low-correlating solutions (i.e., a sleeve) within a traditional portfolio can help it to better withstand a variety of adverse market conditions.

Inflation and rising rates may be the topic du jour today, but market conditions continually change, and new threats may surface tomorrow or years from now.

Instead of trying to pinpoint when a threat will occur and making just-in-time allocation calls, investors may be better served by modernizing their overall diversification approach with an allocation to a blend of low-correlating strategies that can do well in different environments – an approach designed to add resilience to portfolios by capitalizing on the unique strengths of each strategy as events or changing market environments occur.

The Questions You Should Be Asking

Rather than spending time asking whether a new market risk such as inflation is real or transitory, advisors should ask these questions:

What are the near-term and long-term risks I am concerned about?

Should these risks occur, is there a portfolio shortfall from holding only equity and fixed income?

Can I show my clients what I’ve done within their portfolio to address potential risks?

Is there anything in the portfolio that would actually benefit from the perceived threat?

And most important:

If a particular market condition happens, will any of my clients fall short of reaching their goals?

When an advisor blends different strategies and asset classes that are uncorrelated to equity and fixed income, they can answer these questions with confidence. The key, however, is to think about these issues proactively. Proper diversification should be a constant mindset, not a reaction. By evolving portfolio construction to include a more diverse set of strategies and asset classes, advisors may create a client experience with better outcomes and less volatility.

Past performance does not guarantee future results. Diversification does not assure a profit, nor protect against loss in a declining market. Consumer Price Index measures the variation in prices paid by typical consumers for retail goods and other items. Index performance is not illustrative of Fund performance. One cannot invest directly in and index.

Mutual fund investing involves risk. Principal loss is possible. The Funds are non-diversified, meaning it may concentrate its assets in fewer individual holdings than a diversified fund. Therefore, the Funds are more exposed to individual stock volatility than a diversified fund. The Funds invest in foreign investments and foreign currencies which involve greater volatility and political, economic and currency risks and differences in accounting methods. These risks are greater for emerging markets. The Funds may make short sales of securities, which involves the risk that losses may exceed the original amount invested. Investing in commodities may subject the Funds to greater risks and volatility as commodity prices may be influenced by a variety of factors including unfavorable weather, environmental factors, and changes in government regulations. Investing in derivative securities derive their performance from the performance of an underlying asset, index, interest rate or currency exchange rate. Derivatives can be volatile and involve various types and degrees of risks, and, depending upon the characteristics of a particular derivative, suddenly can become illiquid. Derivative contracts ordinarily have leverage inherent in their terms which can magnify the Fund’s potential for gains or losses through increased long and short position exposure. The Fund may access derivatives via a swap agreement. A risk of a swap agreement is the risk that the counterparty to the agreement will default on its obligation to pay the Fund. Investments in debt securities typically decrease in value when interest rates rise. This risk is usually greater for longer-term debt securities. Investments in Asset Backed, Mortgage Backed, and Collateralized Mortgage-Backed Securities include additional risks that investors should be aware of such as credit risk, prepayment risk, possible illiquidity and default, as well as increased susceptibility to adverse economic developments. The LoCorr Long/Short Equity Fund may invest in small- and medium-capitalization companies which involve additional risks such as limited liquidity and greater volatility. The Fund may also invest in lower-rated and non-rated securities which present a greater risk of loss to principal and interest than higher-rated securities. ETF investments are subject to investment advisory and other expenses, which will be indirectly paid by the Fund. As a result, the cost of investing in the Fund will be higher than the cost of investing directly in ETFs and may be higher than other mutual funds that invest directly in stocks and bonds. ETFs are subject to specific risks, depending on the nature of the ETF. The Spectrum Income Fund’s portfolio will be significantly impacted by the performance of the real estate market generally, and the Fund may be exposed to greater risk and experience higher volatility than would a more economically diversified portfolio. Property values may fall due to increasing vacancies or declining rents resulting from economic, legal, cultural, or technological developments. Investments in Limited Partnerships (including master limited partnerships) involve risks different from those of investing in common stock including risks related to limited control and limited rights to vote on matters affecting the Limited Partnership, risks related to potential conflicts of interest between the Limited Partnership and the Limited Partnership’s general partner, cash flow risks, dilution risks and risks related to the general partner’s limited call right. Underlying Funds are subject to management and other expenses, which will be indirectly paid by the Fund.

Click here for important disclosure and definition information.

Mutual fund investing involves risk. Principal loss is possible.

The Fund’s investment objectives, risks, charges and expenses must be considered carefully before investing. The prospectus contains this and other important information about the investment company, and it may be obtained by clicking here or a free-hard copy is available by calling 1.855.LCFUNDS. Read it carefully before investing.

The Funds are offered only to United States residents, and information on this site is intended only for such persons. Nothing on this website should be considered a solicitation to buy or an offer to sell shares of the Funds in any jurisdiction where the offer or solicitation would be unlawful under the securities laws of such jurisdiction.

The LoCorr Funds are distributed by Quasar Distributors, LLC.

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful.

Strictly Necessary Cookies

Strictly Necessary Cookie should be enabled at all times so that we can save your preferences for cookie settings.

If you disable this cookie, we will not be able to save your preferences. This means that every time you visit this website you will need to enable or disable cookies again.